Most corporate net-zero plans are written to be believed. Very few are built to be audited.

The gap between those two things is what independent verification exposes. When we worked with a large Indian industrial conglomerate to technically audit their 2040 net-zero transition plan, the strategy document was thorough and well-structured.

Over the last few years, net-zero announcements became almost standard across large corporations. Targets for 2040, 2050, and even earlier began appearing in annual reports. But as regulatory scrutiny increases, a more difficult question is emerging: Can these commitments actually survive technical verification?

That is where many organizations are discovering a major gap between ambition and operational reality. A company may genuinely intend to decarbonize. But intention alone does not create an audit-ready climate claim. What matters increasingly is whether: emissions baselines are measurable, reduction pathways are traceable, and offsets can withstand independent scrutiny.

What the document did not contain was verifiable data. Baseline emissions for the anchor year were reconstructed from partial utility records. Efficiency improvement projections used manufacturer performance specs rather than measured operational outcomes.

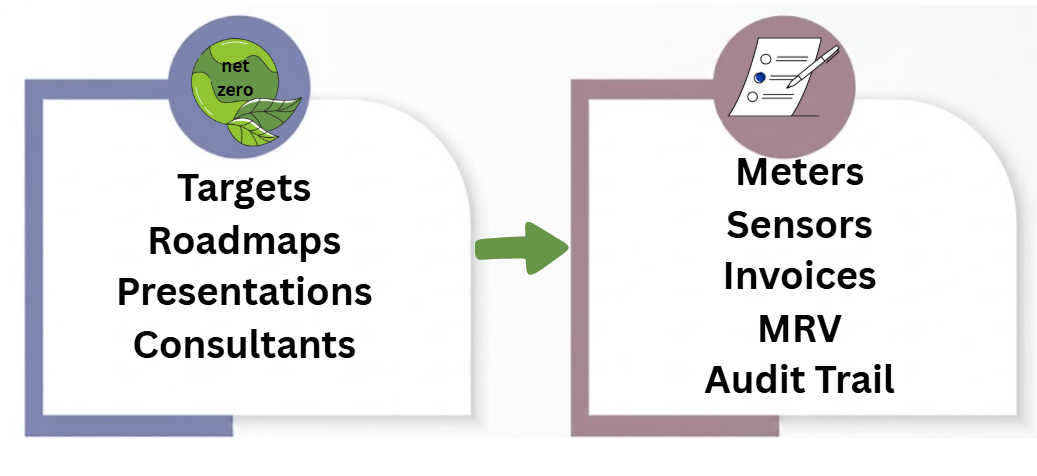

The Gap Between Strategy and Data

A well-written net-zero strategy and an auditable net-zero plan are different documents. The first explains what a company intends to do; the second provides a data trail connecting every claimed reduction to a measured outcome.

This distinction is becoming more important because climate disclosures are moving closer to financial disclosure standards. Historically, roadmaps relied on estimated trajectories and consultant assumptions. That was acceptable when ESG was a reputational exercise.

But once BRSR Core, CSRD, and climate-linked financing enter the equation, assumptions become risky. Auditors increasingly expect source-level evidence, operational traceability, and timestamped monitoring. A climate target without supporting data infrastructure is increasingly viewed as incomplete.

Written to be believed by stakeholders. Relies on industry averages and consultant projections. Often lacks connection to real-time operational systems.

Built to be verified by regulators. Uses direct activity data and facility-level monitoring. Every reduction is backed by a verifiable digital audit trail.

The problem is not that narrative strategies are useless. Strategic planning remains important because companies need transition pathways and technology roadmaps. The issue arises when narrative confidence exceeds measurement capability.

Many companies currently know where they want to reach, but cannot continuously prove where emissions actually stand today. That creates a credibility gap that becomes visible during technical audits.

Scope 3: Where Most Plans Break Down

For industrial companies, Scope 3 is not a secondary concern. It is the majority of the problem. Value chain emissions typically represent 85 to 90 percent of total impact.

Scope 3 remains the hardest part of corporate decarbonization because it sits outside direct operational control. Suppliers, logistics, and raw material extraction collectively represent the majority of emissions, yet most companies still rely heavily on questionnaires or spend-based estimates.

These methods provide directional visibility, but they rarely capture real operational variation across suppliers. Two suppliers producing similar materials may have completely different energy sources and process efficiencies. Without direct measurement, these differences remain invisible.

Rigorous Scope 3 verification requires moving from questionnaire-based supplier engagement to actual emissions data from supplier facilities. For raw material suppliers with significant land-use footprints, satellite monitoring provides an objective external check.

This is where verification infrastructure becomes strategically important. As disclosure standards mature, large companies may increasingly require suppliers to provide facility-level emissions records and verifiable operational data. Suppliers capable of producing transparent carbon data may gain competitive advantages in procurement.

Why Climate Claims Are Entering The Audit Era

Corporate climate reporting is following a path similar to financial reporting. What began as voluntary disclosure is increasingly becoming subject to assurance, verification, and regulatory oversight. Investors are no longer satisfied with high-level commitments alone.

This shift changes how net-zero strategies are evaluated. The question is no longer whether a company has announced a target. The question is whether progress toward that target can be independently demonstrated using reliable evidence.

As regulations mature, climate claims may increasingly require audit-quality controls similar to those applied to financial information. Companies building verification systems today are likely to adapt more effectively than those relying on retrospective reporting exercises.

The Offset Liability Most Companies Carry Unknowingly

Every net-zero plan has a residual gap hard-to-abate emissions addressed through offset procurement. Registry certification represents only one layer of evaluation.

Offsets create a unique risk because companies assume registry certification automatically guarantees long-term integrity. In reality, a project may still face permanence risk or baseline inflation even if it initially passed methodology requirements.

This creates a hidden liability. If a company claims climate neutrality using offsets later questioned by regulators or investors, the reputational and financial consequences extend far beyond the original cost. Many organizations are beginning to treat offset procurement as forensic risk assessment.

Confirms a project followed an approved methodology at registration. Does not confirm current accuracy or additionality on the ground. A minimum acceptable check.

Uses satellite monitoring to verify additionality and baseline accuracy in real-time. Confirms offsets represent claimed reductions.

The market is slowly moving toward a hierarchy of offset quality. Credits backed by continuous monitoring and transparent geospatial evidence are increasingly separated from generic registry-issued credits with limited visibility.

What Audit-Ready Net-Zero Looks Like

A net-zero plan that can survive independent scrutiny is built differently. The baseline is constructed from operational data systems, and reduction targets are connected to measurable parameters.

One of the clearest patterns emerging is that companies with strong operational data systems adapt much faster. The challenge becomes much harder when emissions data is fragmented across spreadsheets and vendor estimates. The technical difficulty is not calculating emissions; it is building a defensible evidence chain.

Operational Baseline: Data constructed from utility meters and MES systems, not reconstructed from annual invoices.

Continuous Monitoring: Reduction targets connected to measurable parameters tracked in real-time to detect deviations early.

Verified Scope 3: Moving beyond questionnaires to direct supplier facility data and satellite-based land-use monitoring.

Project-Level Due Diligence: Offsets selected based on independent technical verification of additionality and permanence.

Audit Pipeline: A continuous digital audit trail ready for regulatory assurance under BRSR Core or CSRD.

Continuous monitoring matters because decarbonization pathways rarely progress in perfectly linear ways. Facilities change fuel mixes and alter production intensity over time. Without continuous visibility, companies may not detect divergence between projected reductions and actual outcomes until long after reporting cycles close.

Why Carbon Data Is Becoming Corporate Infrastructure

The next phase of corporate decarbonization will be defined less by target announcements and more by data infrastructure. Companies increasingly require systems capable of collecting, validating, storing, and reporting emissions information across facilities and supply chains.

Carbon data is becoming operational infrastructure. The organizations that invest in measurement capabilities today will be better positioned to meet future assurance requirements, financing expectations, and procurement standards.

This shift mirrors the evolution of financial reporting. Reliable accounting systems eventually became mandatory business infrastructure. Carbon measurement systems are moving in a similar direction.

The Future of Corporate Climate Strategy

The broader market environment is changing rapidly. Investors and regulators are becoming more sensitive to climate claim credibility. Net-zero commitments are no longer evaluated only on ambition. They are increasingly evaluated on measurement quality and audit readiness.

In many ways, the market is moving from: “Who has the boldest target?” to: “Who can prove progress most reliably?”

The future of corporate climate strategy will likely belong to organizations that treat verification as core infrastructure.

A net-zero target without measurable evidence may still create headlines. But a net-zero pathway supported by operational data, continuous monitoring, and independently verifiable outcomes creates something far more valuable: credibility under scrutiny.

As climate regulation tightens, the distinction between “declared ambition” and “provable transition” will define which corporate strategies survive.

Assess Your Net-Zero Readiness

Is your organization ready for the shift from narrative strategy to auditable data? Contact the Sylithe policy desk for a net-zero readiness assessment and dMRV scoping session.

Key Takeaways & Metrics

A summary of the core concepts discussed in this article.

| Concept | Relevance | Impact Level | Status |

|---|---|---|---|

| Methodology | Core to accurate MRV | High | Active |

| Integrity | Essential for credit value | Critical | Mandatory |

| Technology | Enables scale | High | Growing |

Data synthesized from Sylithe Research.