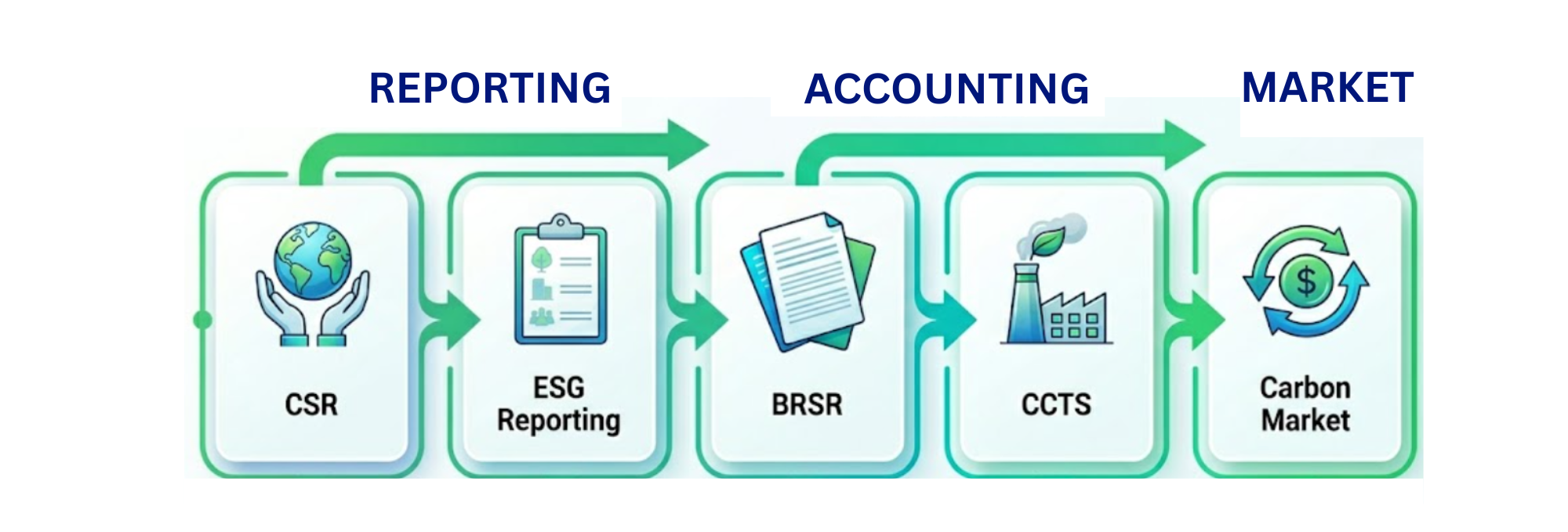

For a decade, Indian companies filed sustainability reports. Under CCTS, they will trade on them.

India's Carbon Credit Trading Scheme changes the underlying logic of corporate ESG. A sustainability claim is no longer a communication decision it is a financial position. What was acceptable in a BRSR disclosure is not acceptable in a traded asset.

India Is Moving From Disclosure to Carbon Accounting

For most Indian companies, ESG historically functioned as a disclosure exercise. CCTS changes that assumption fundamentally. Once carbon reductions become tradable market instruments, emissions data stops being a communications metric and becomes a financial accounting variable.

The transition is comparable to the historical evolution from informal bookkeeping to regulated financial accounting standards. India is building the institutional infrastructure to transform carbon into an auditable economic commodity.

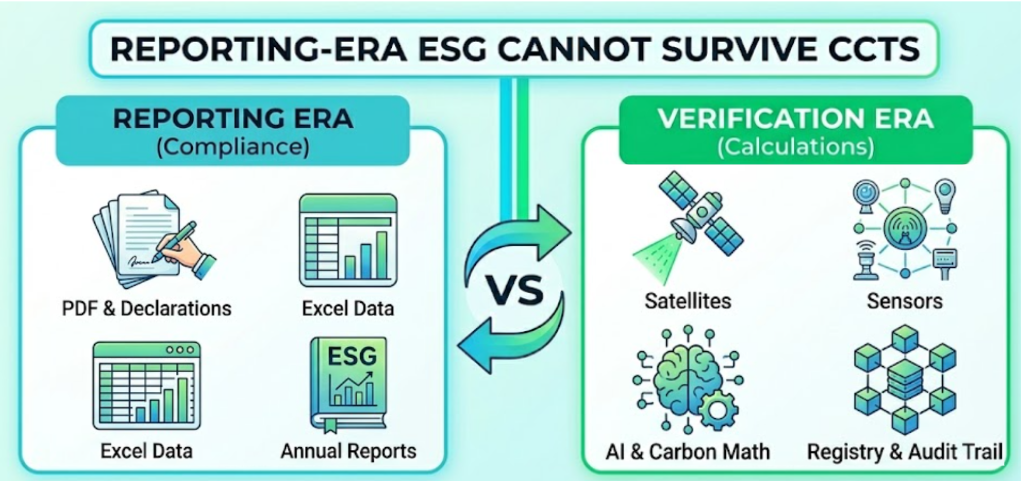

Why Reporting-Era ESG Cannot Survive CCTS

The ESG reporting model was designed for reputational management. CCTS changes the stakes entirely. Any discrepancy in the underlying data is no longer a reporting error it is a question of financial fraud.

Why Carbon Markets Require Much Higher Precision

Voluntary ESG disclosures tolerate a degree of approximation. Carbon markets cannot. A regulated market requires every issued carbon credit to represent a real, measurable, and verifiable reduction.

The market shifts from “Did the company disclose emissions?” to “Can the company prove emissions reductions continuously and independently?” That distinction defines the next-generation carbon economy.

The Difference Between ESG Reports And Carbon Assets

The distinction between an ESG report and a carbon asset is subtle but extremely important. An ESG report is primarily an information product. Its purpose is to communicate environmental performance, sustainability initiatives, governance practices, and risk management activities to investors, regulators, customers, and other stakeholders. The value of the report lies in transparency and disclosure. While accuracy matters, the report itself is not a tradable economic instrument.

A carbon credit operates differently. It is not merely a statement about environmental performance; it is a market asset that can be bought, sold, retired, or used to satisfy compliance obligations. Every credit represents a quantified environmental outcome. If that outcome cannot be demonstrated with evidence, the asset itself becomes questionable. In financial markets, investors do not purchase a company simply because it publishes a report. They purchase assets supported by verifiable records, audit trails, and enforceable standards. Carbon markets follow the same logic.

This shift has major implications for Indian companies preparing for CCTS. Under a disclosure-based ESG framework, firms could focus on annual reporting cycles and sustainability narratives. Under a carbon market framework, they must focus on measurement accuracy, monitoring frequency, data governance, and verification procedures. The market is no longer asking whether a company has a sustainability strategy. It is asking whether the company can continuously prove the environmental outcomes it claims to generate.

Trust therefore becomes infrastructure rather than reputation. Buyers, regulators, auditors, and financial institutions need confidence that every issued carbon credit corresponds to a real and measurable reduction in emissions. That confidence comes from transparent methodologies, independent verification systems, traceable data sources, and continuous monitoring. Companies that build these capabilities early will be better positioned to compete in India’s emerging carbon economy, while those relying solely on traditional ESG reporting frameworks may find themselves unprepared for a market where environmental claims carry direct financial consequences.

“An ESG report communicates performance. A carbon credit monetizes performance. The difference is verification.”

— Sylithe Research

Why Carbon Data Is Becoming Financial Data

For decades, emissions data existed primarily inside sustainability reports. It was reviewed by ESG teams, discussed in annual disclosures, and consumed by stakeholders interested in corporate responsibility. Under emerging carbon market frameworks such as CCTS, that role is changing. Carbon data is increasingly becoming financial data because it directly influences the creation, valuation, and transfer of economic assets.

The comparison to financial accounting is useful. Investors would never accept a company claiming revenue without invoices, audit trails, or supporting documentation. Carbon markets operate on the same principle. Every issued carbon credit represents a measurable environmental outcome. If that outcome cannot be supported by reliable evidence, the market value of the asset becomes questionable.

This shift places greater importance on carbon inventories, emissions measurement systems, and verification controls. What was once considered a sustainability metric is increasingly treated as an economic variable that can influence enterprise value, financing access, regulatory exposure, and market competitiveness.

The concept of carbon liabilities is also becoming more important. Companies that underestimate emissions, fail verification requirements, or cannot support reduction claims may face financial consequences ranging from compliance costs and market penalties to reduced investor confidence. Carbon accounting is therefore moving closer to financial accounting in both rigor and consequence.

“The future of carbon markets depends on treating environmental data with the same discipline used for financial data.”

— Sylithe Research

Carbon Is Becoming a Strategic Corporate Variable

Under CCTS, decarbonization projects increasingly become economic optimization decisions. Carbon efficiency gradually becomes a source of competitive advantage rather than merely a reporting benefit.

“A carbon credit is a financial instrument first. Its environmental value is only as credible as the data infrastructure behind it.”

— Sylithe Research

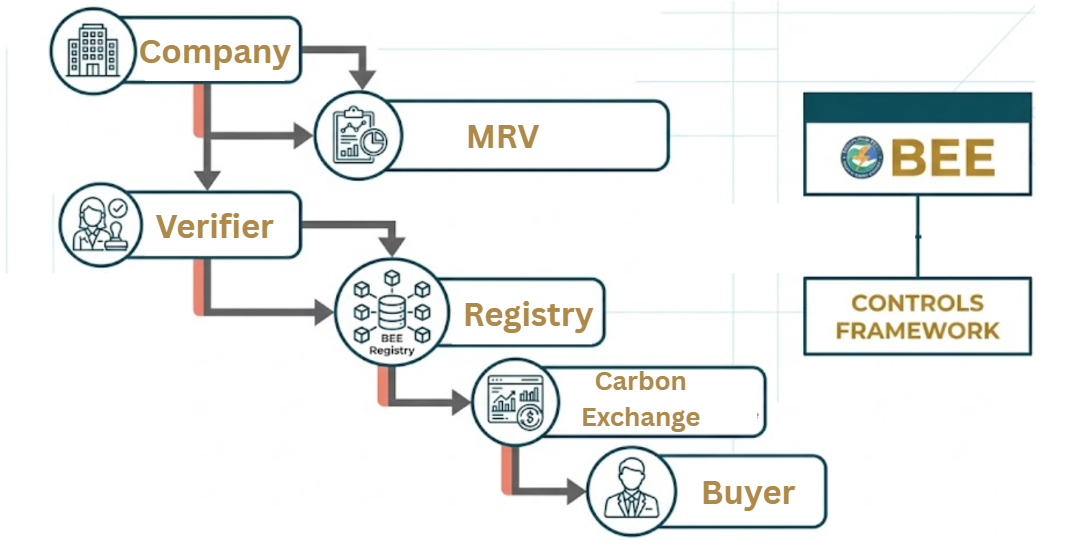

BEE's Design Logic: Fungibility and Centralization

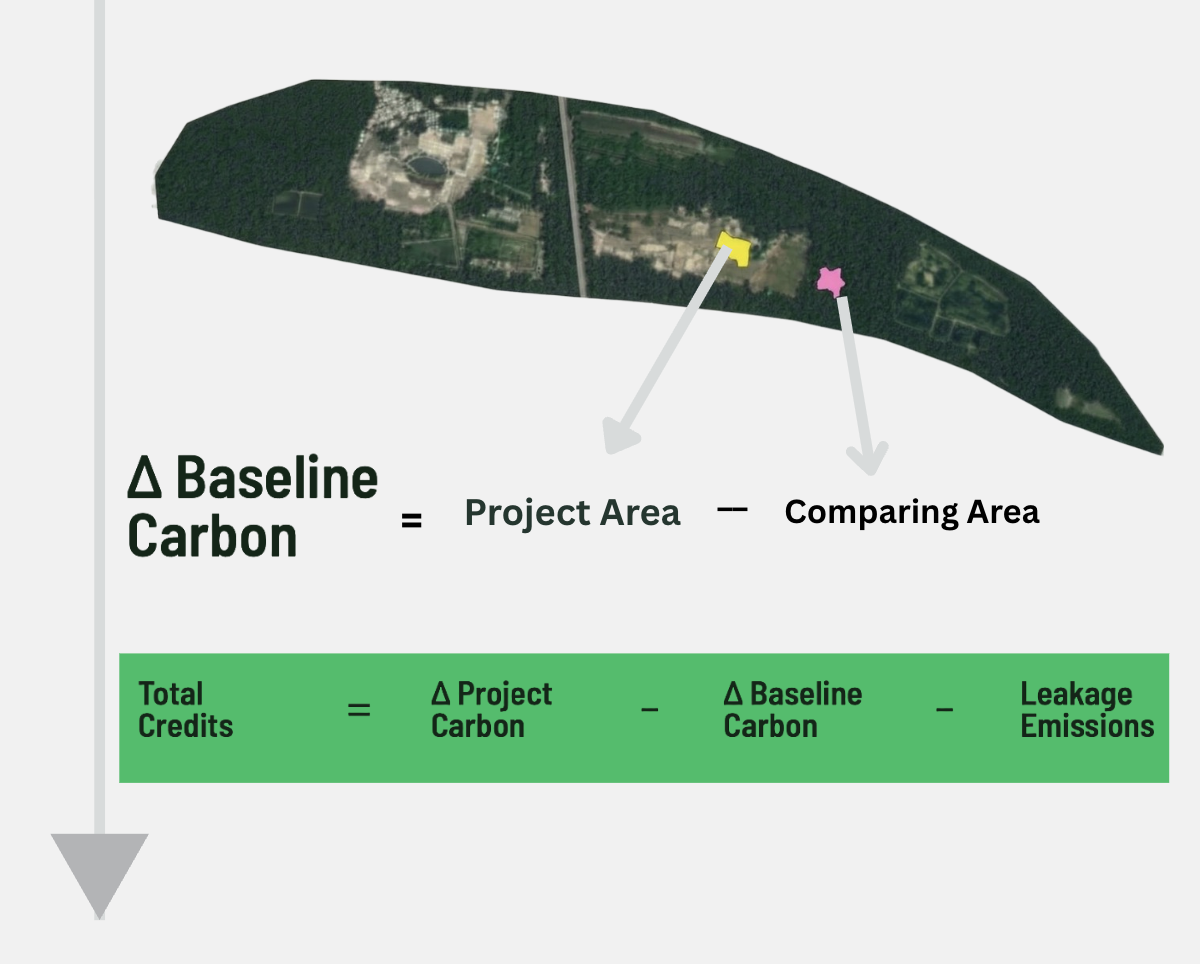

For a carbon market to be liquid, credits must be fungible. BEE is building toward a centralized registry that tracks every credit from issuance to retirement, with sector-wide baselines replacing individual project baselines.

Why BEE Is Standardizing the Market

BEE is effectively attempting to create a nationally interoperable carbon accounting architecture. Sector-wide baselines and centralized registries reduce variability and improve market confidence.

India’s long-term ambition involves integration with broader global carbon finance systems and cross-border climate trade mechanisms.

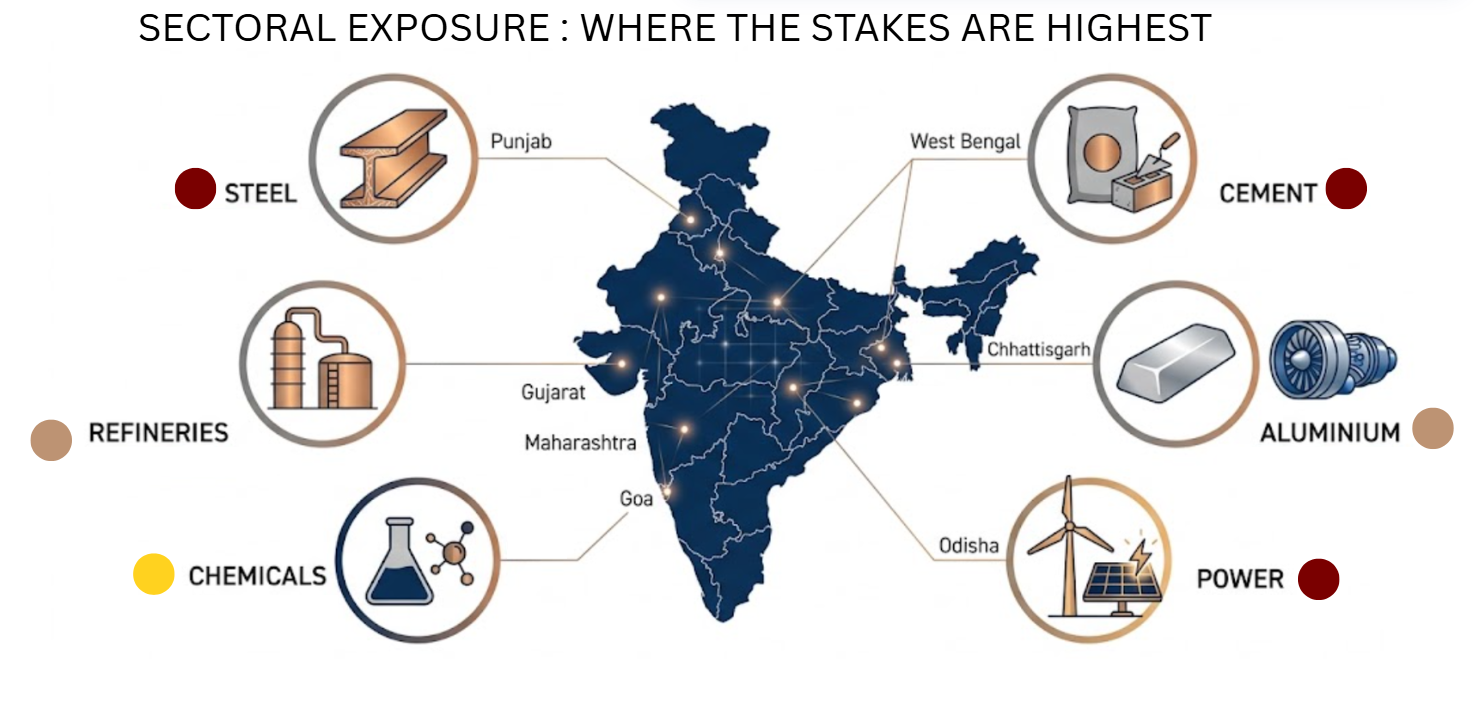

Sectoral Exposure: Where the Stakes Are Highest

CCTS begins with obligated entities in energy-intensive sectors like steel, cement, and aluminum. For these sectors, the proof requirement demands physical evidence, not just project documentation.

Why Industrial Sectors Face the Greatest Exposure

Heavy industry carries both high emissions intensity and high export sensitivity. For these firms, carbon intensity may soon influence export competitiveness and financing access.

CBAM Changes the Economics of Exporting

The EU’s CBAM transforms carbon reporting into a trade issue. Exporters increasingly need independently verified emissions data and traceable audit trails to maintain access to European markets.

Why Exporters Cannot Ignore Verification

For exporters, carbon verification is no longer a sustainability discussion. It is becoming a trade requirement. International buyers increasingly demand visibility into emissions performance across supply chains, particularly in sectors exposed to climate regulations and procurement standards.

European buyers are under growing pressure to understand the carbon intensity of imported goods. This requirement extends beyond final manufacturers to suppliers, subcontractors, logistics providers, and raw material producers. Companies unable to provide credible emissions information may find themselves at a competitive disadvantage.

Supply chain transparency is becoming a strategic capability. Buyers increasingly want evidence rather than declarations. They want to know how emissions were measured, what methodology was used, whether the data was independently verified, and whether supporting documentation can withstand scrutiny.

As climate regulations evolve, trade competitiveness may depend not only on product quality and price but also on the credibility of carbon accounting systems. Verification infrastructure is rapidly becoming part of market access infrastructure.

Verification Is Becoming A Trade Requirement

The companies best positioned for future export markets will be those capable of proving emissions performance through independently verifiable data systems.

The Cost Of Bad Carbon Data

Poor carbon data carries costs that are often underestimated. In a disclosure-driven environment, inaccurate reporting may result in reputational concerns. In a regulated carbon market, the consequences are more direct. Errors in emissions calculations, unsupported reduction claims, and weak audit trails can affect asset value, compliance status, and market credibility.

One of the most common risks is credit rejection. Verification bodies and market participants increasingly scrutinize supporting evidence. If underlying data cannot be validated, credits may face delays, discounts, or outright rejection.

Audit failures represent another challenge. As markets mature, auditors are expected to demand stronger evidence chains, clearer methodologies, and greater transparency around data collection processes. Organizations relying on fragmented spreadsheets or manual workflows may struggle to meet future expectations.

The market also imposes pricing consequences. Buyers generally assign lower value to assets carrying higher uncertainty. Projects supported by strong monitoring and verification systems often command higher confidence and potentially stronger pricing than projects with weak evidence frameworks.

Bad Data Creates Real Economic Risk

In carbon markets, uncertainty is not merely a reporting issue. It becomes a pricing issue, a compliance issue, and potentially a financial issue.

What Verification Infrastructure Must Look Like

The verification layer required is continuous, satellite-based, and independent. Sylithe's platform provides a multi-sensor satellite stack with AI-led anomaly detection.

Why Continuous MRV Replaces Periodic Audits

Environmental conditions change continuously, not annually. Real-time sensors and satellite imagery allow verification systems to operate continuously, providing the dynamic evidence infrastructure markets expect.

Data Provenance Becomes Critically Important

The important question is becoming: “Who controls the underlying data generation process?” Independent verification infrastructure reduces selective reporting risk and ensures baseline integrity.

The Future of India’s Carbon Economy

CCTS represents the beginning. Over time, the market may expand toward Article 6 trading and sovereign climate market integration. The distinction between “reported emissions” and “verified emissions” will become increasingly important.

- Continuous satellite monitoring replaces annual point-in-time audits

- AI anomaly detection flags gaps between claimed and observed performance

- Independent data provenance removes developer control over verification inputs

- Output is a live evidence trail, not a static document

The Rise Of Carbon Assurance

The evolution of carbon markets is beginning to resemble the historical development of financial reporting. Decades ago, investors relied heavily on company-provided information with limited independent validation. Over time, audit requirements, assurance standards, and regulatory frameworks emerged to improve trust. Carbon markets appear to be following a similar path.

Assurance is becoming increasingly important because environmental claims now influence economic decisions. Investors, buyers, regulators, lenders, and trading platforms all require confidence that reported outcomes are accurate. Independent assurance provides a mechanism for creating that confidence.

Traditional sustainability reporting often relied on periodic reviews. Future carbon markets are likely to demand continuous evidence generation. Satellites, IoT sensors, industrial monitoring systems, automated reporting platforms, and AI-assisted analytics are transforming how assurance is performed.

Third-party assurance providers are also expected to play a larger role. Their function extends beyond verification of individual projects. They contribute to overall market confidence by ensuring methodologies are applied consistently and that reported outcomes are supported by objective evidence.

This trend aligns closely with the direction of CCTS. As carbon credits become more integrated into financial decision-making, market participants will increasingly expect audit-quality controls, traceable data lineage, and independently verifiable monitoring systems.

In the long term, the distinction between carbon assurance and financial assurance may narrow significantly. Both disciplines exist for the same reason: to transform information into trusted economic infrastructure. The companies that recognize this shift early will be better prepared for a future in which environmental performance carries measurable financial value.

“Carbon assurance is not an additional compliance layer. It is the trust layer upon which future carbon markets will operate.”

— Sylithe Research

CCTS represents the financialization of environmental performance inside the Indian economy.

Emissions data is no longer a static sustainability disclosure. It becomes tradable economic infrastructure. The companies that succeed will be the ones capable of continuously proving their claims with independently verified evidence systems.

India’s next carbon economy will ultimately be built not only on decarbonization itself, but on the credibility of the data used to measure it.

How Sylithe supports CCTS readiness

We help Indian companies build the verification infrastructure needed to operate in a regulated carbon market: continuous monitoring, independent data provenance, and audit-ready evidence trails. Contact our policy desk to secure your 2026 compliance roadmap.

Key Takeaways & Metrics

A summary of the core concepts discussed in this article.

| Concept | Relevance | Impact Level | Status |

|---|---|---|---|

| Methodology | Core to accurate MRV | High | Active |

| Integrity | Essential for credit value | Critical | Mandatory |

| Technology | Enables scale | High | Growing |

Data synthesized from Sylithe Research.