Carbon offset markets operate on a fundamental wager: that the carbon sequestered today will remain locked away for decades. But for nature-based solutions, the promise of permanence is far more fragile than the certificates suggest.

The phrase 'nature-based solution' is doing enormous rhetorical work. Trees grow slowly, die suddenly, and exist within ecosystems facing accelerating disruption from the very climate crisis they are meant to help solve. When a corporation retires a carbon credit and claims to have 'offset' its emissions, it is betting that a particular patch of forest will remain standing, unburned, unlogged, and undisturbed not just for this year, but for the duration of the atmosphere's need.

That is not a small bet. And in many cases, it is one that markets are losing. For technology-based solutions like Direct Air Capture (DAC), which mineralizes CO₂ into rock formations, the wager has geological timescales behind it. But for the forests, wetlands, and grasslands that dominate the voluntary carbon market (VCM), permanence is a probabilistic claim masquerading as a certainty.

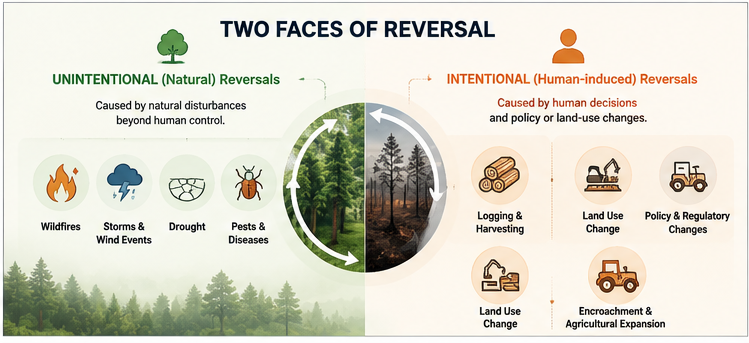

The Two Faces of Reversal

To understand permanence, we must first disaggregate 'reversal risk' the umbrella term for events that return sequestered carbon to the atmosphere. Beneath it lie two structurally distinct categories, each requiring different interventions:

Natural disasters wildfires, pest and beetle outbreaks, tropical storms, flooding that are being directly amplified in frequency and severity by climate change itself. Projects cannot fully prevent these events; they can only absorb and disclose their consequences.

Human decisions that deliberately end a project: commercial logging driven by timber price spikes, shifts in government land-use policy, illegal encroachment and deforestation, and the collapse of conservation easements when institutional oversight weakens.

The distinction matters enormously for insurance design. Unintentional reversals are, in principle, random events that can be pooled across a portfolio similar to how reinsurance treats catastrophic weather events. Intentional reversals are systemic risks tied to governance, land tenure security, and economic incentives. Pooling them together, as the current market largely does, obscures the difference in how they should be priced and prevented.

"The market treats a wildfire and a logging decision as the same category of loss. They are not. One is an act of nature; the other is an act of governance failure."

The Bootleg Fire and the Limits of Buffer Pools

In the summer of 2021, the Bootleg Fire tore through southern Oregon, eventually consuming more than 400,000 acres an area roughly twice the size of New York City. Within that landscape were forest parcels enrolled in carbon offset programs and credited to corporate buyers including Microsoft and BP.

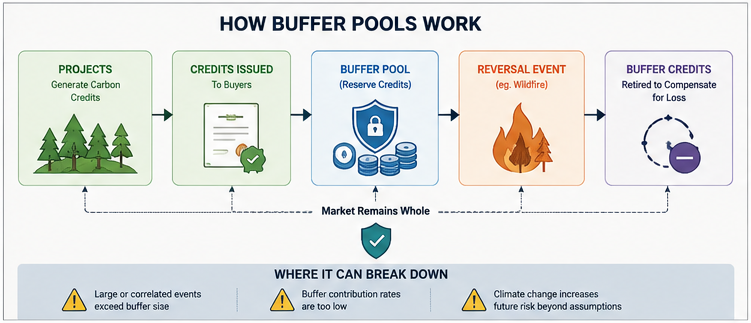

These projects had, as required, contributed a percentage of their issued credits to a centralized 'buffer pool' managed by their registry. The buffer pool is the market's primary insurance mechanism: credits withheld from sale, held in reserve against exactly this kind of catastrophic reversal event. When a project burns down, buffer pool credits are retired to keep buyers whole the buyer's offset remains on the books even though the underlying forest is gone.

The Bootleg Fire did not break the buffer pool. But it illuminated a looming structural question: given that climate change is making extreme fire seasons the norm rather than the exception across forested North America, and given that the same climate trajectory affects forest projects globally and simultaneously, are buffer pools large enough to survive the next decade?

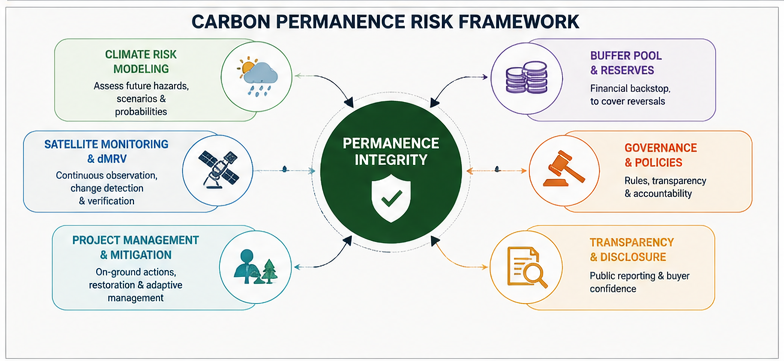

How Buffer Pools Work and Where They Break Down

When a nature-based project is validated and begins issuing credits, the registry assigns it a risk rating based on factors including fire history, biodiversity, governance, and tenure security. A project with elevated risk might be required to contribute 20–30% of its credits to the communal buffer pool. A well-governed, low-risk project in a stable jurisdiction might contribute as little as 10%.

In theory, this is an elegant mutual insurance structure. In practice, it contains several embedded assumptions that are increasingly strained. The current system relies on risk ratings determined at project inception and re-evaluated on cycles of roughly five years by manual auditing teams. This is systematically misaligned with how risk actually behaves in nature:

A drought in year two materially increases wildfire probability in year three. But a project’s buffer contribution, set at inception, remains fixed. The market is collecting premiums calibrated to conditions that no longer exist.

Manual verification teams visit sites on multi-year cycles. Small-scale illegal clearing five hectares here, twelve there is routinely missed between cycles, accumulating into material undetected reversals. By the time auditors return, the evidence may have been replanted or obscured.

Political instability, election of governments with different land-use priorities, or changes to indigenous land rights can transform a low-risk project into a high-risk one overnight. Static ratings have no mechanism to respond to these cliff events between audit cycles.

Risk ratings are largely assigned per-project, without sufficient modeling of how losses in one region correlate with losses in others under shared climate scenarios. Buffer pools may be individually adequate while being collectively insufficient.

Why 100-Year Permanence Is So Difficult To Guarantee

One of the most overlooked realities in carbon markets is that permanence commitments often outlive the institutions that create them. A project developer may exist for ten years. A corporate buyer may change strategy after five years. Governments may change through multiple election cycles. Yet the permanence obligation remains attached to the carbon outcome for decades. This mismatch between institutional time horizons and atmospheric time horizons creates a structural challenge that cannot be solved through paperwork alone.

The atmosphere does not care whether a reversal occurs in year five or year seventy. Carbon released back into the atmosphere has the same climatic impact regardless of when it occurs. This is why long-term carbon storage remains one of the most important indicators of environmental integrity and one of the most difficult promises for project developers to guarantee.

Many carbon standards require storage periods approaching 100 years. While this duration is necessary from a climate perspective, guaranteeing ecological stability over multiple generations is extraordinarily difficult. Forest ownership changes, political priorities evolve, climate conditions shift, and economic incentives fluctuate.

A forest protected today may face completely different risks twenty, fifty, or eighty years from now. Droughts, heat waves, pests, invasive species, infrastructure development, and land-use pressures all compound over time. As a result, permanence should be viewed as a continuously managed risk rather than a one-time certification outcome.

The Permanence Gap: What Buyers Don't Know

Why Permanence Risk Is Becoming A Financial Risk

Historically, permanence was treated as a technical issue discussed primarily by auditors and registry specialists. That is no longer the case. Carbon buyers increasingly evaluate permanence risk because it directly influences credit quality, reputation, and future liability. A reversal event can affect not only environmental outcomes but also investor confidence and corporate climate claims.

As carbon markets mature, permanence risk is becoming a pricing variable. Credits supported by stronger monitoring systems, lower reversal probabilities, and transparent risk disclosures are increasingly viewed as higher-quality assets. This trend mirrors financial markets where investors demand higher returns from assets carrying greater uncertainty.

Corporate buyers purchasing offsets from large brokers or exchange platforms typically receive a certificate, a project description, and a verification report. What they rarely receive is any ongoing information about whether the project is still intact. An offset purchased in 2019 may carry zero indication, in 2026, that the underlying forest experienced a partial reversal event in 2022.

This information asymmetry is not accidental. Registries disclose buffer retirements, but these disclosures are technical documents consulted primarily by specialists. The project pages that buyers reference are rarely updated between verification cycles. A buyer doing standard due diligence would have no visibility into whether their specific project had experienced intervening disturbance.

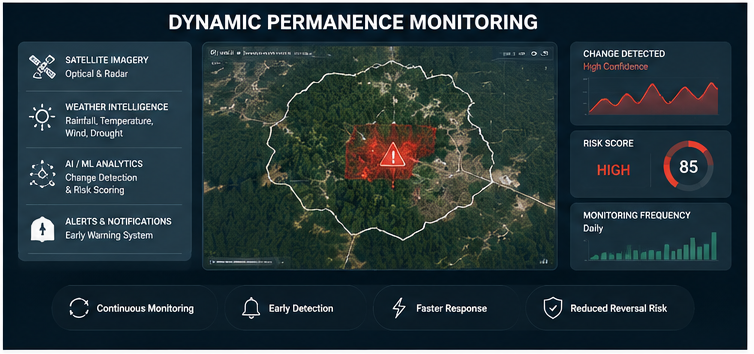

Dynamic Permanence Monitoring: A Different Architecture

Modern digital MRV systems integrate satellite imagery, radar observations, weather intelligence, machine learning, and automated alerts into a single monitoring architecture. Instead of relying exclusively on field visits, projects can now be evaluated continuously, dramatically improving transparency and responsiveness.

The response to a static, audit-driven system is continuous, satellite-based monitoring that replaces the 5-year verification cycle with near-real-time disturbance detection. The underlying technology is now mature: synthetic aperture radar can detect canopy changes through cloud cover; optical imagery has reached sub-meter resolution at daily cadence; machine learning models can flag anomalies at scale that no human team could review.

Applied to carbon monitoring, this capability unlocks an alert system rather than an audit system a shift in fundamental architecture. Rather than waiting for an auditor to visit a site and document what has changed, algorithms scan daily satellite feeds and generate alerts when detected change exceeds a threshold.

Are Buffer Pools Actually Solvent?

The question facing the voluntary carbon market is not whether reversals will occur. They already do. The real question is whether existing reserve systems are large enough to absorb future losses under a warming climate. Many current buffer pool models were designed using historical risk assumptions that may underestimate future fire intensity, drought frequency, and ecosystem stress.

Researchers increasingly focus on correlation risk. Traditional insurance assumes losses occur independently. Climate-driven disturbances challenge this assumption because droughts, heatwaves, and wildfires can affect multiple projects simultaneously across entire regions. This creates pressure on reserve pools that were not originally designed for synchronized loss events.

As a result, many experts expect future carbon markets to adopt dynamic buffer requirements that adjust continuously based on observed environmental conditions rather than static assessments conducted every few years.

The Buyer's Checklist: Questions That Matter

For organizations purchasing nature-based offsets, the following questions directly probe permanence quality and the answers should be required elements of any offset procurement process:

What is the specific buffer pool contribution percentage for this project, and how was the risk rating determined? Ask for the methodology, not just the number. Projects contributing less than 15% without strong supporting rationale warrant scrutiny.

Is there a third-party early warning system in place for fires, illegal clearing, or other disturbance events? Who operates it, at what cadence, and what is the protocol when an alert is triggered?

Does the registry have a documented history of buffer pool retirements, and at what scale? A registry that has never needed to retire buffer credits has either very good projects or very little transparency.

Is the project's risk rating reviewed dynamically, or only on a fixed cycle? Under what circumstances would the buffer contribution be increased before the next scheduled audit?

What is the project's land tenure structure, and under what legal framework is the conservation easement or land protection held? Projects dependent on voluntary landowner commitments without binding legal instruments carry elevated intentional reversal risk.

In the event of a partial reversal, how would you be notified, and on what timeline? The answer to this question reveals whether the seller's monitoring infrastructure is real or nominal.

"Permanence is not a binary state to be certified once and forgotten. It is a monitored risk a probabilistic claim about the future behavior of complex ecological and social systems. Markets that treat it as a checkbox are not pricing permanence; they are pricing the appearance of it. The difference will become clearer, and more consequential, with every fire season."

Key Takeaways & Metrics

A summary of the core concepts discussed in this article.

| Concept | Relevance | Impact Level | Status |

|---|---|---|---|

| Methodology | Core to accurate MRV | High | Active |

| Integrity | Essential for credit value | Critical | Mandatory |

| Technology | Enables scale | High | Growing |

Data synthesized from Sylithe Research.