India’s natural capital is its biggest climate asset. By 2030, nature-based solutions will be a larger driver of rural economic growth than traditional commodities.

For years, Nature-Based Solutions (NbS) were seen as a 'Nice-to-Have' a small niche for CSR projects or boutique carbon buyers. In 2026, that has changed. NbS is now a strategic industrial sector, attracting billions in institutional capital and playing a central role in India's sovereign climate strategy.

India has the biological and social potential to supply 20% of the world's high-integrity nature-based credits. But the market has matured. The days of 'Plant-and-Forget' projects are over. The 2026 landscape is defined by 'High-Resolution Observability', 'Community-Led Governance', and 'Institutional-Grade Finance'.

This article is a strategic outlook on the four 'Super-Sectors' of Indian NbS, the impact of the domestic compliance market, and why the 'Integrity Revolution' is the best thing that ever happened to Indian forest and land-use projects.

Why India Is Uniquely Positioned for NbS Leadership

India possesses one of the world's most diverse ecological landscapes, ranging from Himalayan forests and mangroves to grasslands and agroforestry systems. Combined with a large rural workforce and growing climate policy support, this creates a unique foundation for large-scale nature-based solutions.

Unlike many countries that rely heavily on a single ecosystem type, India can generate carbon benefits across multiple landscapes simultaneously. This diversity reduces risk and creates opportunities for different project categories, buyers, and investment models.

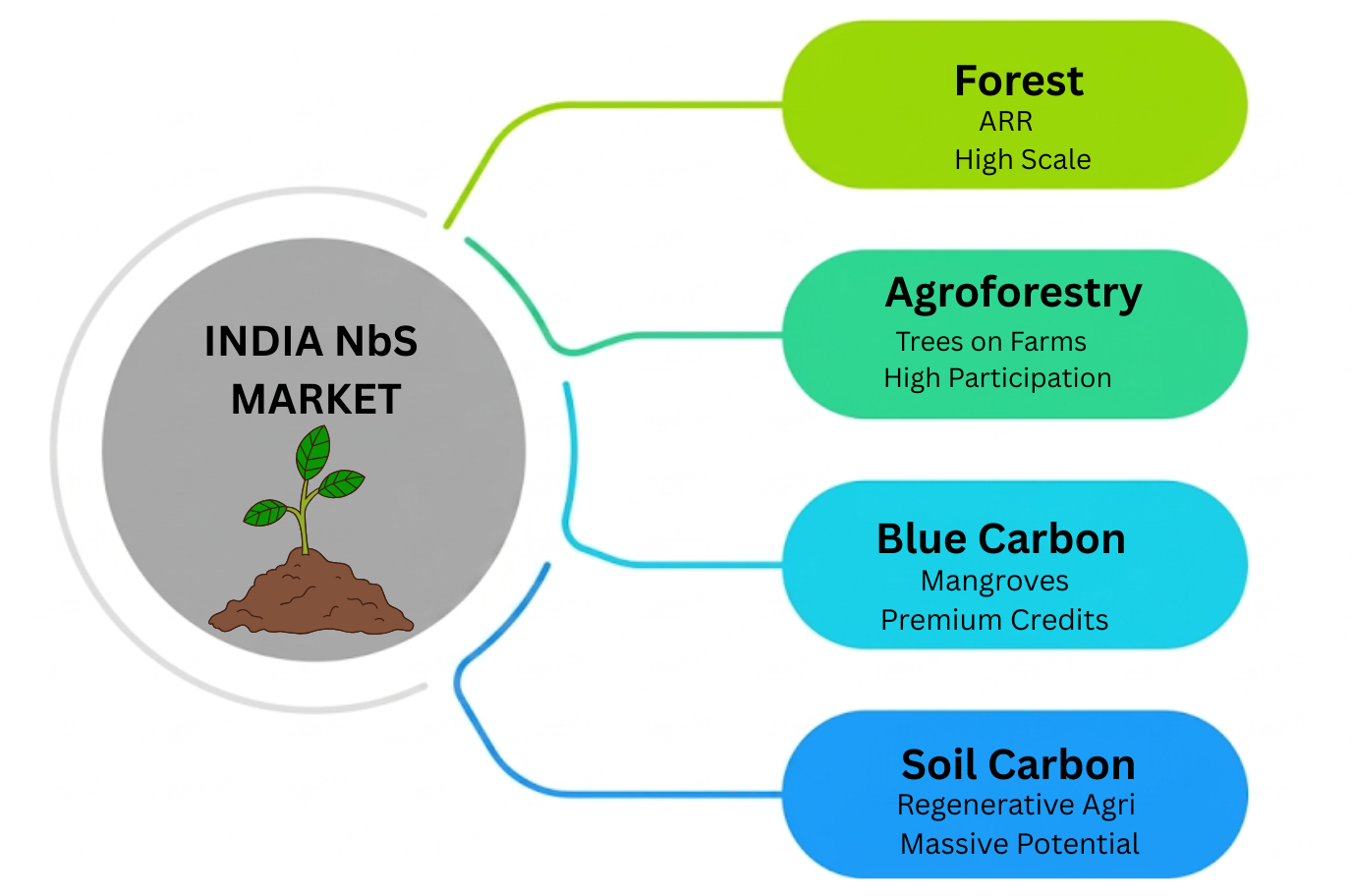

The Four Super-Sectors of Indian NbS

We identify four sectors that will drive 80% of the NbS value in India over the next decade.

1. Large-Scale Forest Restoration (ARR)

Current Opportunity: Focused on the Western Ghats, Central India, and the Northeast. The shift is away from monoculture plantations toward 'Native Species Restoration'. These projects are being integrated with the Forest Rights Act (FRA) to ensure communities are the long-term stewards of the carbon stocks.

Key Challenges: Securing large contiguous land parcels without legal disputes; navigating complex government forestry regulations; high initial capital expenditure before credits are issued.

Future Outlook: Public-private partnerships will accelerate, with state governments leasing degraded land to private developers who bring institutional capital and advanced MRV.

2. Smallholder Agroforestry

Current Opportunity: More than half of India's agricultural landscape contains scattered trees that are not formally counted in forest inventories. These trees represent a significant carbon sink that can be monetized through high-quality carbon projects.

Key Challenges: Fragmented land ownership, farmer onboarding, high data collection costs, and long verification timelines for dispersed millions of trees.

Future Outlook: AI-powered tree detection and satellite monitoring are making it possible to aggregate millions of farm trees into investable carbon assets, turning agroforestry into a primary driver of regenerative agriculture.

3. Blue Carbon (Mangroves and Seagrass)

Current Opportunity: The highest-value credits in the market. Focused on the Sundarbans, the Odisha coast, and Gujarat. These projects are funded by buyers who need 'Coastal Resilience' co-benefits alongside intense carbon sequestration.

Key Challenges: Vulnerability to extreme weather events (cyclones); complex tidal zone land ownership; specialized measurement required for below-ground biomass.

Future Outlook: Blue carbon will command the highest premium in the Indian market, driven by intense corporate interest in verifiable biodiversity and resilience impacts.

4. Soil Organic Carbon (SOC)

Current Opportunity: The largest untapped pool. Transitioning India's vast agricultural lands to low-tillage, high-carbon practices is the 'Holy Grail' of Indian NbS.

Key Challenges: Permanence risk (a farmer ploughing once can release years of stored carbon); extremely high soil sampling costs to prove additionality.

Future Outlook: With new digital MRV pipelines and hybrid remote-sensing models, soil carbon is finally becoming a bankable asset, scaling across the Indo-Gangetic plain.

The Economics of NbS: Why Investors Are Increasingly Interested

Nature-based solutions are attracting institutional investors because they generate multiple value streams:

- Carbon credits

- Biodiversity benefits

- Water security improvements

- Community livelihood enhancement

- Climate adaptation outcomes

Unlike traditional environmental projects, NbS initiatives can generate measurable and recurring financial returns, creating a robust asset class for the 2026 climate economy.

The Impact of the CCTS: A Permanent Domestic Demand

The launch of the Indian Carbon Market (ICM) and the CCTS has changed the risk profile of NbS projects. Previously, developers were dependent on the volatile international voluntary market. Today, they have a 'Floor Price' set by domestic compliance demand.

The 294 'Designated Consumers' (DCs) the giants of Indian steel, cement, and power have a statutory obligation to meet emission intensity targets. While they will invest in process efficiency, many will need to purchase NbS offsets to cover their final 5-10% shortfall. This creates a multi-billion rupee annual demand for Indian forest and soil credits, independent of global price swings.

Role of Technology in NbS: The Rise of Digital Monitoring

Modern NbS projects rely heavily on advanced technology:

- Satellite imagery for real-time monitoring

- AI-based land classification

- LiDAR for canopy structural measurement

- Drone surveys for ground-truthing

- Blockchain registries for transparent tracking

- Digital MRV systems for automated compliance

Technology is reducing verification costs while improving transparency, making projects scalable and audit-ready from day one.

Why the Integrity Revolution Matters

The 'Carbon Credit Crash' of 2023 was a painful but necessary correction for India. It weeded out low-quality developers and forced the industry to adopt better MRV. In 2026, 'Integrity' is no longer a buzzword; it is a technical specification.

Before 2023: Weak monitoring, inconsistent methodologies, and low buyer confidence plagued the market.

After 2023: The adoption of dynamic baselines, continuous monitoring, and better verification has led to higher-quality credits. Stronger standards actually increase long-term market value.

- dMRV as Standard: Projects without real-time satellite monitoring are now effectively un-fundable.

- Article 6 Alignment: Developers are ensuring their projects are "A6-Ready" to access the high-premium international transfer market.

- FRA Compliance: Respecting community rights is now a core requirement for ICVCM CCP labels.

| Feature | Conventional Project | High-Integrity Project |

|---|---|---|

| Price Potential | Lower | Higher |

| Investor Interest | Mixed | Institutional |

| Monitoring | Periodic field sampling | Continuous dMRV + satellite monitoring |

| Community Participation | Variable | Transparent benefit sharing |

| Compliance Readiness | Basic | Audit-ready |

| Buyer Confidence | Moderate | High |

Challenges That Still Remain: The Constraints to Scaling

While the potential is vast, scaling Nature-Based Solutions (NbS) in India involves navigating a complex landscape where ecological ambition often collides with systemic barriers. Recent research into India's carbon sequestration efforts highlights several critical constraints that developers and investors must overcome.

Institutional and Governance Gaps

A primary hurdle is fragmented management. NbS implementation frequently suffers from siloed operations across various government departments—such as forestry, agriculture, and water resources. This fragmentation leads to duplicated efforts and coordination difficulties. Furthermore, there is a distinct lack of clear, standardized regulatory frameworks for NbS, creating jurisdictional confusion between national and state mandates, which often results in prolonged project delays.

Additionally, researchers note a significant 'Data Deficit.' The absence of high-resolution, localized ecological, climate, and biodiversity data (such as comprehensive forest inventories or localized heat maps) hampers evidence-based decision-making. Without this baseline data, designing robust, verifiable projects becomes incredibly difficult.

Economic and Financial Barriers

Despite the desperate need for massive investment, there remains a significant gap in adaptation finance. Many of the crucial co-benefits of NbS—such as improved soil health, biodiversity conservation, and water filtration—are difficult to value in immediate, liquid market terms. This makes it challenging to build strong, bankable business models that traditional financiers can understand.

The market maturity is also a factor. Institutional investors often face difficulty performing due diligence for NbS projects compared to traditional 'grey' infrastructure (like solar or wind farms). The diversity, site-specific nature, and biological risks (like fire or disease) of natural projects require specialized financial instruments and insurance products that are currently nascent in the Indian market.

Technical and Social Dimensions

On the technical side, the absence of unified design protocols means that consultants and project leads often have to recreate frameworks from scratch for each new site. This severely limits the speed at which solutions can be scaled. There is also a noted shortfall in trained personnel—including ecologists, remote-sensing engineers, and local government officials—capable of designing and monitoring high-integrity NbS.

Socially, the success of NbS in India increasingly relies on being 'locally-led.' Top-down projects that fail to secure social acceptance often face sabotage or failure. Deep integration with traditional knowledge and strict adherence to the rights of indigenous and local communities (such as compliance with the Forest Rights Act) is not just ethical—it is a practical prerequisite for permanence. The risk of 'green grabbing' or threats to local biodiversity highlight the need for careful, rights-based planning to ensure carbon sequestration does not come at the cost of local livelihoods.

- Land tenure complexity and ambiguous historical rights

- Siloed government departmental coordination

- Lack of standardized design and MRV protocols

- Financing gaps for early-stage project development

- Valuation of non-carbon co-benefits (biodiversity, water)

- Carbon price volatility in the transition to compliance markets

Vision 2030: India’s NbS Outlook

By 2030, India could emerge as one of the largest suppliers of high-integrity nature-based credits globally. Growth will be driven by increasing domestic demand, Article 6 markets, digital MRV adoption, and large-scale ecosystem restoration programs.

This creates opportunities not only for carbon project developers but also for investors, corporates, state governments, and local communities.

Conclusion: Building a Nature-Positive India

The scale of the opportunity is matched only by the scale of the responsibility. We are not just building a market; we are re-financing the restoration of our national ecosystems. For the first time in history, the economics of conservation are beating the economics of extraction. That is the true story of NbS in India in 2026.

In the carbon market of 2026, India is no longer a follower; it is the laboratory where the world’s most advanced nature-based solutions are being built.

Deploy your NbS capital

Sylithe provides the technical and regulatory infrastructure for high-integrity NbS deployment in India. We combine institutional-grade dMRV with deep expertise in CCTS and Article 6 compliance. If you are ready to scale your impact across India's natural capital, let's talk.